Mortgage Calculator AL (Alabama)

Overview of Alabama Housing Market 2025

The Alabama housing market has shown resilience in 2025, following a cooling period in 2023. Home prices in Alabama have increased by 4.1% year-over-year, with the median price now at $281,400. Despite a decrease in the number of homes sold, the market remains competitive, supported by a strong economy and a growing population.

In February 2025, there were 24,093 homes for sale in Alabama, marking a 10.1% increase from the previous year. The number of newly listed homes was 6,013, slightly down by 3.3% year-over-year. The median days on the market have increased to 73 days, indicating a more balanced market.

If you are thinking about buying a home in Alabama in 2025, it is important to be aware of these trends and understand your budget.

At Brighton Bank, our commitment goes beyond just providing financial services. We believe in empowering our customers with the tools and resources they need to make informed decisions about their financial future. That's why we've put together this dedicated mortgage calculator landing page – to offer you a seamless, transparent, and personalized way to explore your home financing options.

What's on this page?

-Mortgage Calculator

-Property Tax in Alabama

-Closing Costs in Alabama

-Housing Market in Alabama

-Mortgage Resources

-Terminologies

Mortgage Calculator AL (Alabama)

How to Calculate a Mortgage Payment

Calculating a mortgage payment involves a few key components: the loan amount, interest rate, loan term, and the type of mortgage. The most common type of mortgage is a fixed-rate mortgage, where the interest rate remains constant throughout the loan term. Here's how to calculate your monthly mortgage payment: The formula to calculate the monthly mortgage payment is:

M = P * [r(1+r)^n] / [(1+r)^n - 1]

The Variables are as follows:

-

M is the monthly mortgage payment.

-

P is the principal loan amount.

-

r is the monthly interest rate (annual rate divided by 12 and converted to a decimal).

-

n is the number of monthly payments (loan term in years multiplied by 12).

How a Mortgage Calculator can help you.

The Mortgage Calculator AL (Alabama) is a powerful tool designed to assist individuals in making well-informed decisions about their home financing options. This calculator provides a range of benefits:

Payment Estimation: Predict your monthly mortgage payments based on loan details, aiding budget planning.

Scenario Comparison: Testing different loan amounts, interest rates, and terms to understand their effects on payments.

Loan term: Choose 30 years for lower monthly payments but higher interest or 15 years for less interest with higher monthly payments.

Avoiding strain: Brighton Bank's calculator factors taxes, insurance, and mortgage costs for a clear monthly commitment view.

Down payment: Lower 3% down payments feasible, calculator assists in optimal initial investment.

Affordability Assessment: Determining how much house you can comfortably afford within your budget.

Interest Analysis: This shows the total interest paid over the loan's life, guiding decisions on loan terms and types.

Key Determinants of Your Mortgage Payment

At Brighton Bank, we understand that your mortgage payment is influenced by a range of factors. Here are the essential elements that contribute to shaping your mortgage payment:

-

Loan Amount and Interest Rate: The total amount you borrow and the interest rate applied directly impact your monthly payment. A higher loan amount or interest rate typically results in higher monthly payments, while a lower loan amount or interest rate leads to more manageable payments.

-

Loan Term and Type: The length of your loan term and whether it's a fixed-rate or adjustable-rate mortgage matters. Shorter terms often have higher monthly payments but lower overall interest costs. In contrast, longer terms may offer lower monthly payments but potentially higher interest expenses over time.

-

Property-Related Costs: Property taxes based on your home's value and location, along with homeowners insurance to safeguard your investment, are included in your monthly payment. We can help you estimate these costs accurately.

-

Down Payment and PMI: A larger down payment reduces your loan amount, potentially lowering your monthly payment. If your down payment is less than 20 percent, Private Mortgage Insurance (PMI) might apply, adding a cost to your payment until you gain sufficient equity.

Our team at Brighton Bank is committed to guiding you through these intricacies, ensuring you make informed decisions tailored to your financial aspirations. With our expertise, you can navigate these elements and secure a mortgage payment that suits your unique needs.

What you can do to lower your monthly payment

A mortgage constitutes a long-term financial arrangement aimed at funding a home purchase, necessitating both repayment of the principal amount and the regular settlement of interest to the lender. The monthly cost of a mortgage can vary significantly based on factors like property price, location, and the type of loan selected.

To assist you in curbing your monthly mortgage expenses and achieving savings, Brighton Bank offers insightful strategies:

-

Opt for a more budget-friendly home: Selecting a less expensive property translates to a reduced loan amount and subsequently lowers your monthly mortgage obligation.

-

Make a larger down payment: If you make a down payment of 20% or more, you won't have to pay private mortgage insurance (PMI). PMI is an extra insurance that lenders require if your down payment is less than 20%. It can add hundreds of dollars to your monthly mortgage payment.

-

Secure a lower interest rate: Engage in thorough research across different lenders to identify the most favorable interest rate, contributing to a decreased overall mortgage expense.

-

Adjust your loan term: Opting for a longer loan term results in more manageable monthly payments, though it leads to a higher cumulative interest payment over time.

How lenders decide how much you can afford to borrow

When considering your borrowing capacity, Brighton Bank takes into account several key factors to ensure a responsible and suitable lending decision. Here's how Brighton Bank determines your borrowing capacity:

Income Evaluation: Brighton Bank assesses your income stability and sources to gauge your ability to comfortably make repayments.

Debt-to-Income Ratio (DTI): The bank analyzes your existing debts in relation to your income to determine a borrowing amount that maintains a manageable debt load.

Credit History Check: Your credit score and history are reviewed to judge your creditworthiness and ensure that the borrowing terms align with your financial track record.

Down Payment & Affordability: Brighton Bank considers your down payment amount, overall property expenses, and the chosen loan type to ensure that the borrowing amount remains within your financial means.

Determining Your Affordable Home Budget in AL (Alabama)

To determine your affordable home budget in Alabama, you will need to consider your income, other debt obligations, down payment, housing costs, and other living expenses. Lenders will typically qualify you for a mortgage payment that is no more than 28% of your gross monthly income and 36% of your total monthly debt obligations, including your housing costs. The median home price in Alabama is $207,145.

Meet Sarah, a prospective first-time homebuyer in Alabama. With a gross income of $60,000, she aims to spend 28% ($1,400) on housing, factoring in her $800 monthly debts. Including her $1,200 expenses, she estimates a max mortgage payment of $1,400. After getting pre-approved, Sarah feels confident in her budget, ensuring a balanced financial approach as she ventures into the local housing market

Once you have an estimate of your monthly mortgage payment, you can start to look at homes that fit your budget. It is important to keep in mind that your monthly mortgage payment is not the only cost of homeownership. You will also need to factor in property taxes, homeowners insurance, and maintenance and repairs.

Buying a home is a big decision, so it is important to do your research and make sure that you are financially prepared. Remember that affordability is not only about the numbers but also about your comfort level with the financial commitment. Owning a home comes with additional costs beyond the mortgage, such as maintenance and repairs, so it's important to leave room in your budget for unexpected expenses.

Next Steps: What to Do After You Have Estimated Your Mortgage Payments

Following your estimation of mortgage payments, the journey towards homeownership unfolds with essential next steps guided by Brighton Bank.

Whether you're embarking on this path for the first time, considering refinancing, or managing credit challenges, Brighton Bank is here to offer invaluable support at every phase.

-

Compare Our Rates: Before making a commitment, it's crucial to explore and assess offers from various mortgage providers. Brighton Bank encourages you to compare our rates with others, ensuring you make an informed decision. For more details, you can also access information about mortgage rates tailored to your location.

-

Undecided? Rent or Buy: If you're still weighing the options between renting and buying a home, Brighton Bank provides the guidance you need to evaluate which choice best suits your unique circumstances and financial goals.

-

Expand Your Knowledge: Brighton Bank provides a comprehensive resource to help you expand your understanding of diverse mortgage options. Whether you're interested in reverse mortgages, VA home loans, or FHA home loans, Brighton Bank equips you with insights to select the mortgage type that aligns with your preferences and requirements.

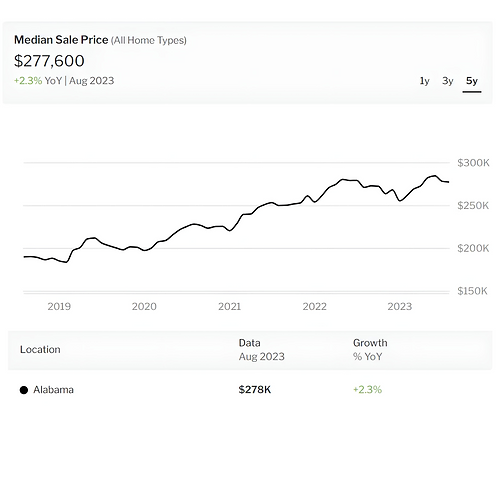

A significant transformation is underway in the Alabama housing market. In April 2023, there was a notable 0.65% decrease in the median sale price compared to the previous year, accompanied by a substantial 24.3% drop in the number of homes sold. With the gradual decline of mortgage rates, currently at 6.79%, a new wave of buyers is entering the market. While the Alabama housing market is showing signs of revival, it's not without its challenges, including the looming potential of interest rate hikes and the risk of a housing market recession.

Source: Redfin Housing Market Data

Source: Redfin Housing Market Data

The economy's performance has surpassed initial expectations, leading to an increase in the 10-year Treasury yield and subsequent higher mortgage rates. The 30-year fixed-rate mortgage has now crossed the seven percent threshold, a level last observed in November. Despite facing challenges of affordability, demand has felt the effects. Yet, the primary reason for the slowdown in home sales remains the persistently low inventory. While some economists anticipate a deceleration in the housing market for 2023, they don't foresee a crash. The recent banking crisis caused mortgage rates to fluctuate, but they are currently stabilizing. This stability has bolstered buyer confidence, prompting more individuals to consider entering the housing market.

In July 2023, the median home price in Alabama experienced a marginal increase of 0.001% compared to the previous year, reaching a median price of $279,800. The average number of homes sold demonstrated a decline of 16.9% year over year. In specific terms, there were 5,166 homes sold in July this year, representing a decrease from the 6,218 homes sold in July of the previous year. The median duration that homes stayed on the market was 38 days, marking an 8-day increase compared to the previous year.

What is the housing market like right now?

What does this mean?

The trajectory and speed of fluctuations in home prices serve as indicators of the housing market's vigor and the evolving affordability of homes. Presently, the median home price in the United States stands at $279,800.

Source: Redfin Housing Market Data

Average Closing Cost in AL (Alabama) Counties

When buying a home in Alabama, it's crucial to consider not only the purchase price but also the closing costs associated with the transaction. Closing costs encompass a variety of fees and expenses that are typically paid at the closing of the real estate deal. These costs can vary significantly depending on the county in which you're purchasing the property.

Average closing costs are the fees and expenses that homebuyers and sellers typically incur during the process of closing a real estate transaction. These costs can vary widely depending on factors like location, property value, and the specific terms of the deal. On average, closing costs typically range from 2% to 5% of the home's purchase price. For a homebuyer, these costs can include expenses such as loan origination fees, appraisal fees, title insurance, property taxes, and attorney fees. Sellers, on the other hand, may be responsible for costs like real estate agent commissions, transfer taxes, and any outstanding liens or repairs required to close the sale.

The exact breakdown of closing costs can differ from one transaction to another, but certain fees are fairly standard across most real estate transactions. These can include lender fees, title insurance, and escrow fees. It's essential for both buyers and sellers to carefully review the estimated closing costs provided by their real estate professionals and lenders to have a clear understanding of the financial implications of the transaction. Homebuyers may also have the opportunity to negotiate some of these costs with the seller or lender, potentially reducing their financial burden during the closing process.

The average closing costs encompass a range of fees and expenses incurred when buying or selling a property, and they typically amount to a percentage of the home's purchase price. The specific costs can vary widely depending on various factors, and it's crucial for individuals involved in a real estate transaction to be aware of these costs and to review and negotiate them whenever possible. Understanding closing costs is a fundamental aspect of the homebuying or selling process and helps individuals budget effectively for the overall cost of their real estate transactions

Average Property Tax in AL (Alabama) Counties

Understanding average property taxes in different Alabama counties is crucial for homeowners and investors. It helps assess affordability, make county comparisons, plan finances, and guide investment choices. This knowledge informs budgeting, decision-making, and potential returns on real estate investments.

Source: US Census Bureau 2020 American Community Survey,National Association of Realtors, SmartAsset

The dataset provides valuable insights into the property tax landscape of several counties, offering a glimpse into the diverse financial considerations associated with property ownership across different regions. Notably, the median home values vary significantly, with some counties like Autauga and Baldwin boasting higher values of $161,200 and $211,600, respectively, while others like Bullock and Barbour exhibit lower median home values of $74,800 and $86,500.

These variations in median home values have a direct impact on the corresponding median annual property tax payments. Counties with higher median home values, like Autauga and Baldwin, also have relatively higher median annual property tax payments of $480 and $765, respectively. Conversely, counties with lower median home values, such as Bullock and Barbour, feature more moderate median annual property tax payments of $408 and $327.

Another crucial factor to consider is the average effective property tax rate, which reflects the proportion of a property's value that is paid in property taxes. Interestingly, counties like Bullock and Calhoun, with median home values on opposite ends of the spectrum, have comparable average effective property tax rates at 0.55% and 0.51%, respectively. This suggests that while the value of the property significantly influences tax payments, the tax rate itself also plays a role in the overall tax burden.

In summary, this dataset underscores the intricate relationship between property values, property tax payments, and average effective property tax rates. It highlights the varying degrees of property tax burden experienced by homeowners in different counties, influenced by factors such as home values, local tax policies, and community needs. Understanding these variations can provide valuable insights for homeowners, potential buyers, and policymakers alike when navigating the intricacies of property ownership and taxation within these counties.

What Property Tax Exemptions Are Available in Alabama?

Let's delve into four common property tax exemptions applicable in Alabama:

-

Homestead Exemption: Homeowners who use their property as their primary residence may qualify for exemptions on certain taxes, such as property taxes. It provides a reduction in the assessed value of the property for tax purposes, which ultimately lowers the property tax owed. The amount of the exemption varies by county, but it can significantly reduce the tax burden for homeowners.

-

Senior Citizen Exemption: Seniors aged 65 and older may be eligible for additional property tax relief. The exemption varies by county and may offer further reductions in property taxes for eligible senior citizens.

-

Disabled Veteran Exemption: Disabled veterans in Alabama may qualify for property tax exemptions. The level of exemption can vary based on the veteran's disability rating and the assessed value of the property. This exemption aims to recognize the sacrifices of disabled veterans by reducing their property tax liability.

-

Widows and Widowers Exemption: This exemption is available to surviving spouses of military service members or first responders who died in the line of duty. It offers property tax relief to help ease the financial burden for those who have lost their loved ones while serving their communities or country.

Property Tax Landscape in Alabama and Beyond

Property taxes are a major source of revenue for local governments in Alabama. They are used to fund essential services such as schools, libraries, and parks. The state does not have a statewide property tax, but counties, cities, and towns all levy property taxes on real estate. The amount of property tax that you pay in Alabama depends on the assessed value of your property, the millage rate, and any exemptions that you may qualify for.

The assessed value of your property is the value that is used to calculate your property taxes. It is typically based on the market value of your property, but it can be lower or higher. The millage rate is the percentage of the assessed value of your property that you pay in property taxes. The millage rate varies from county to county and city to city.

Exemptions are reductions in the amount of property taxes that you have to pay. There are many different types of exemptions available in Alabama, including homestead exemptions, disabled veterans exemptions, and farmland exemptions.

The average property tax bill in Alabama is $674 per year. However, the actual amount that you pay can vary significantly depending on the value of your property, the millage rate, and any exemptions that you may qualify for.

Home Insurance

Home insurance, also known as homeowners insurance or property insurance, is a type of insurance policy that provides financial protection to homeowners against various risks and perils that could damage or destroy their property. This insurance coverage helps homeowners recover financially in case of unexpected events that result in damage to their homes, or belongings, or liability for injuries or damages to others that occur on their property.

Coverage Types and Options

When it comes to protecting your most valuable asset, understanding your options is essential. Home insurance offers various types of coverage to ensure you're safeguarded against unexpected events. Here are some key coverage types:

-

Dwelling Coverage: This protects the structure of your home itself, including its foundation, walls, roof, and more.

-

Personal Property Coverage: Covers your belongings, such as furniture, electronics, and clothing, in case of damage or theft.

-

Liability Coverage: Offers financial coverage in the event someone gets hurt on your premises and you are deemed liable.

-

Additional Living Expenses: Helps with temporary housing and living expenses if your home becomes uninhabitable due to covered events.

Factors That Determine Coverage Needs for AL (Alabama)

When considering homeowners insurance in Alabama, there are several factors that will determine the coverage you need. These factors can vary from person to person, but it's important to understand them in order to make an informed decision about your policy. Here are some key factors to consider:

Location - The geographical location of your home is a significant determinant of your coverage needs. Certain areas might be prone to specific risks, such as flooding, hurricanes, or winter storms. Coastal regions, including Mobile and Baldwin counties, are susceptible to flooding and hurricanes, while tornadoes and severe thunderstorms are common in central and northern parts, such as Jefferson County. Winter storms occasionally affect the northern areas, including Madison and Colbert counties, potentially leading to hazardous conditions. Forested regions in the northern and central parts, like Walker and Talladega counties, may experience wildfires during dry periods. Residents and prospective property buyers should remain vigilant, staying informed about weather alerts, preparing for emergencies, and understanding evacuation procedures to minimize the impact of these risks.

Coastal Proximity - Being near the coast can increase the risk of damage from hurricanes and flooding. Special coverage might be needed for these events.

Flood Zones - Homes located in flood-prone areas might require additional flood insurance, as standard homeowners insurance typically doesn't cover flood damage.

High-Crime Neighborhoods - If your home is in an area with high crime rates, your insurance premiums might be higher due to the increased risk of theft and vandalism.

Dwelling Features - The specific features of your home, such as its age, size, construction materials, and overall condition, are crucial in determining coverage. Older homes might have different coverage needs due to potential structural issues or outdated electrical and plumbing systems. Similarly, if you have special features like a swimming pool, a detached garage, or a built-in fireplace, you'll need to ensure these are appropriately covered.

Property Value - The value of your property, including both the land and the physical structure, impacts the amount of coverage you need. It's important to have enough insurance to cover the cost of rebuilding your home if it's damaged or destroyed, which might be different from the market value of the property.

Personal Belongings - Your personal belongings, such as furniture, electronics, clothing, and other possessions, need to be covered against events like theft, fire, or other damage. You'll need to estimate the value of your belongings accurately to ensure you have sufficient coverage. It's a good idea to create a home inventory with detailed descriptions and estimated values of your possessions.

Tips for Lowering Your Homeowners Insurance Premiums for AL (Alabama)

Homeowners in Alabama are often looking for ways to save on their insurance premiums. Here are some helpful tips to lower your homeowner's insurance costs:

-

Shop Around -Don't accept the first insurance quote you get. Instead, compare quotes from multiple companies to find the best deal.

-

Increase Deductibles - A higher deductible means a lower premium. Consider raising your deductible if you have the financial means to cover a higher out-of-pocket expense in case of a claim.

-

Bundle Policies - Many insurance companies offer discounts when you bundle multiple policies, such as homeowners and auto insurance. Inquire about the potential savings when obtaining quotes.

-

Improve Home Security - Installing smoke detectors, burglar alarms, deadbolt locks, and other security measures can reduce the risk of damage or theft, leading to lower premiums. Be sure to inform your insurer once you have implemented these security features.

-

Maintain Good Credit - In many states, including Alabama, insurance companies can use your credit score to determine your premiums. A good credit score can help you save money on your insurance.

-

Stay Claims-Free - Building a claims-free history can often lead to discounts on your premiums. Avoid making smaller claims and save your insurance for significant losses.

By implementing these tips, homeowners in Alabama can potentially enjoy significant savings on their homeowner's insurance premiums while maintaining adequate coverage.

Trends in Homeowners Insurance Rates for AL (Alabama)

Homeowners insurance rates can fluctuate over time due to various factors. Staying informed about the trends in homeowners insurance rates helps homeowners in Alabama make educated decisions regarding their policies. Here are some recent trends worth considering:

-

Increasing Material and Labor Costs - The cost of building materials and labor can impact homeowners insurance rates. In recent years, the rising prices of construction materials and the demand for skilled labor have contributed to an increase in insurance premiums.

-

Climate Change Impact - Climate change can result in an increase in severe weather events, including hurricanes, storms, and floods. These events can cause significant property damage and result in insurance companies adjusting their rates accordingly.

-

Technological Advances - Advancements in technology have led to improved methods of assessing risks and deciding insurance premiums. Insurance companies are increasingly leveraging data and analytics to determine rates, resulting in more accurate pricing based on individual risk profiles.

-

Market Competition - The competitive landscape among insurance companies in Alabama can influence rates. When multiple insurers compete for customers, it can lead to more competitive pricing and potential savings for homeowners.

-

Legislative Changes - Changes in local or state laws can also impact homeowners insurance rates. It's important to stay informed about any regulatory changes that may affect your premiums.

Keeping an eye on these trends helps homeowners in Alabama understand the factors driving insurance rates and make informed decisions when purchasing or renewing their policies.

Average Homeowners Insurance Costs for AL (Alabama)

Understanding the average homeowner's insurance costs in Alabama provides homeowners with a benchmark for comparison. While individual premiums can vary based on numerous factors, here is an overview of the average costs in the state:

In August 2023, the typical expense for homeowners insurance in Alabama is approximately $311 annually, which averages out to around $26 each month. This amount is roughly 82% below the national average of $1,754.

This average cost, however, can vary depending on the factors discussed previously, such as location, dwelling features, property value, and personal belongings.

Homes situated in proximity to certain geographical features, such as coastal areas or flood-prone zones, might command different insurance considerations due to the associated risks.

As is the case with any financial matter, it's crucial to remember that these figures serve as a general guideline and can vary from one homeowner to another. Insurers may consider additional factors such as credit history and discounts for bundling services or installing security systems.

As insurance costs can fluctuate over time, it's advisable to consult with insurance providers to receive accurate quotes tailored to your specific circumstances.

By understanding the average homeowner's insurance costs in Alabama, homeowners can better budget for their insurance expenses and ensure they have appropriate coverage without overpaying.

Alabama Average Insurance Premiums by Dwelling Limit

The provided data offers valuable insights into the property tax structure in Alabama, showcasing the relationship between home values and the corresponding annual tax burdens. In the case of Alabama's property tax data, we see that as income levels increase, the property tax amounts also rise significantly. This progression is evident when comparing the property tax liability of someone earning $250,000, who pays approximately $2,134.81, with someone earning $750,000, who pays approximately $4,960.22. This means that higher-income individuals shoulder a more substantial portion of the property tax burden in the state.

The benefits of progressive property taxation are twofold. First, it ensures that governments have a stable source of revenue to fund essential services such as education, healthcare, infrastructure maintenance, and public safety. Second, it helps mitigate income inequality by placing a relatively smaller financial burden on those with lower incomes. This approach aligns with the principle of vertical equity, which suggests that those who can afford to contribute more should do so to support the common good.

However, progressive property taxation can be a subject of debate and potential challenges. Critics argue that high property taxes on more expensive homes may discourage property ownership and investment in the state. Additionally, the effectiveness of this policy depends on accurately assessing property values and applying consistent tax rates, which can be challenging.

Mortgage Resources in AL (Alabama)

Mortgage resources refer to various tools, information, and support available to individuals seeking to obtain or manage a mortgage loan. Mortgage resources are valuable for both first-time homebuyers and existing homeowners looking to refinance or better understand their mortgage options.

Brighton Bank Mortgage Services

Are you looking for reliable mortgage services in Alabama? Look no further than Brighton Bank! We are dedicated to helping you achieve your homeownership dreams with our range of mortgage solutions tailored to meet your unique needs. Whether you're a first-time homebuyer or a seasoned real estate investor, Brighton Bank is here to assist you every step of the way.

Why Choose Brighton Bank for Your Mortgage Needs?

1. Personalized Service: Our team of experienced mortgage experts will work closely with you to understand your financial goals and find the right mortgage product that fits your budget and lifestyle.

2. Competitive Rates: We offer competitive interest rates and loan terms to help you save money over the life of your loan. Our goal is to make homeownership affordable for you.

3. Simple Pre-Approval Process: Getting started on your homeownership journey is easy with Brighton Bank. You can kickstart the pre-approval process today with just a few simple steps.

Start Your Homebuying Journey with Brighton Bank

Ready to take the first step towards homeownership in Alabama? Click the button below to begin the pre-approval process with Brighton Bank. Our team is excited to work with you and help you achieve your homeownership dreams!

Local Economic Factors in AL (Alabama)

Beyond your mortgage payment, it's essential to consider the local economic factors that can impact your financial stability and property value in Alabama:

Employment Opportunities: The availability of jobs and the health of local industries play a role in your financial security and ability to meet mortgage payments.

Market Trends: Real estate markets can experience fluctuations in prices. Our team can provide you with insights into current market trends to assist in your decision-making.

Infrastructure and Development: Development projects, transportation networks, and infrastructure improvements can affect the desirability and value of properties in certain areas.

Property Value Trends: Understanding how property values have changed over time can give you a sense of the potential appreciation of your investment.

Terms Explained

Using a mortgage calculator is a simple and efficient way to estimate your monthly mortgage payment. By entering essential details like the loan amount, interest rate, and duration of the loan, you can swiftly determine your monthly payments. It's crucial to note:

-

Loan Amount (Principal): This is the total amount of money you're borrowing to purchase the property.

-

Interest Rate: This is the annual interest rate on the loan. Make sure to convert this to a decimal by dividing it by 100.

-

Loan Term: The loan term is the number of years you have to repay the loan. It's usually expressed in years. Typical loan terms are 15, 20, or 30 years. A longer-term typically results in lower monthly payments but more interest paid over time.

-

Down Payment: The down payment is the initial amount of money you contribute toward the purchase price of the home. It's usually a percentage of the home's price, and a larger down payment can result in lower monthly payments.

-

Amortization: Amortization is the process of gradually paying off your mortgage over time through regular monthly payments. Early on, a larger portion of your payment goes toward interest, while later in the loan term, a larger portion goes toward paying down the principal.

-

Closing Costs: These are the fees associated with finalizing the mortgage and completing the home purchase. They can include things like appraisal fees, attorney fees, title insurance, and more.

-

Housing Market: The housing market refers to the buying and selling of residential properties. It includes all the activities and transactions related to homes, apartments, and other types of housing.

-

Mortgage: A mortgage refers to a loan acquired to buy a home, where the property acts as security for the borrowed amount.

-

Private Mortgage Insurance (PMI): A type of insurance that is often required by lenders when a borrower puts down less than 20% of the home's purchase price as a down payment. It's commonly used to mitigate the increased risk associated with lower down payments.

-

Debt-to-Income Ratio: A financial metric used by lenders to assess a borrower's ability to manage their debt payments in relation to their income. The DTI ratio helps lenders evaluate the borrower's financial stability and the likelihood of repaying the loan.